Contact

For whom is the mortgage holiday?

As part of the draft Act on Crowdfunding for Economic Ventures and Borrower Assistance of 10 June, Chapter 10 includes provisions allowing borrowers to take advantage of so-called “mortgage holiday”. The principles laid out in the draft bill show that the mortgage holiday can be used by consumers with mortgage loans granted in PLN (excluding loans indexed and or denominated to a currency other than the Polish currency). The only restriction on the use of the holiday is the indication that it is only available to the consumer in relation to a single contract concluded for the acquisition of a property intended to meet his own residential needs. Loans with a remaining maturity of more than 6 months, granted before 1 July 2022, are subject to payment holiday.

The above conditions indicate a potentially large range of clients who will be able to take advantage of the holiday, restricted only by the definition of the consumer and the non-investment purpose of the loan. What draws attention is the lack of criteria relating to the borrower's situation, which is often raised by the sector as the main objection to the planned legislation.

How does the holidays work?

In line with the draft bill the mortgage holiday will consist in the possibility to “suspend” mortgage payments in the period:

Assuming that the most popular schedule of payments is on a monthly basis, the above conditions make it possible to suspend and postpone 8 mortgage payments in total. What matters is that the project assumes that the suspension of payments cannot be linked with additional fees and the borrower, during the holiday period, will only be required to pay the insurance fees associated with the contract.

Accounting treatment

The currently leading interpretation indicates that there will be a change in the gross carrying amount (GCA) as a result of deferring expected flows, while holding effective interest rate (EIR) constant. This will generate a loss to be recognized in the profit and loss (P&L) account.

This article focuses on the analysis of the amount of this loss leaving aside aspects related to the correct classification of the loss (modification vs. change of estimate) in the P&L or the timing of its recognition (one-time vs. spread over time).

Mortgage loan characteristics

Knowing the general rules and the accounting treatment, it is reasonable to analyse how the characteristics of the loan itself, such as maturity, type of schedule or level of effective interest rate, will affect the level of loss caused by the holiday. While determining the direction of the impact of factors is relatively easy, a detailed sensitivity analysis allows to observe which factors and with what severity will affect the amount of loss.

Although there is no leading interpretation on when to recognize the impact, for the purpose of performing the simulation it was assumed that the entire impact is estimated as of 30 June 2022. Regardless of the type of schedule, a monthly installment payable at the end of the month is assumed.

As a default case, a loan with a residual maturity of 20 years with an equal installment is analyzed. It was assumed that the customer takes full advantage of the mortgage holiday on the first possible dates, in particular from August to November 2022 and at the beginning of the following quarters of 2023. The initially assumed EIR is set to 9%.

In the following sections each assumption will be analysed in terms of its impact on valuation. In order to decouple the analyses from the current value of the mortgage, the impact will be presented as a percentage, where 1% loss for a loan with a gross carrying value of PLN 100 thousand means a negative impact on the result in the amount of PLN 1 thousand.

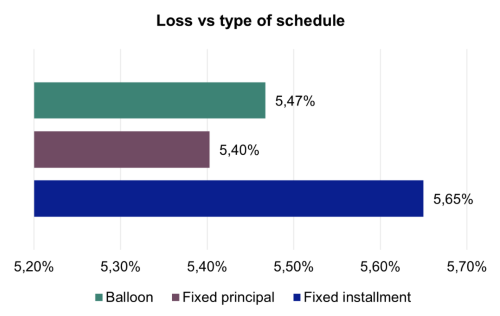

Loss vs type of schedule

The impact of the type of schedule on the loss amount was analysed in the first place. Three types of schedules were analysed: a fixed installment, a fixed principal installment and a balloon payment at the end of the period.

The obtained results indicate that the impact of the type of schedule on the amount of loss is weak. A comparison of the two most common variants shows that the loss in the fixed installment variant is approx. 5% (25 bps) higher than that of the fixed principal installment, due to the earlier repayment of a larger portion of the principal and reduced future interest payments that are deferred. It can also be observed that for theoretical mortgage loans with balloon payment, the far deferral of the principal payment results in a smaller loss that falls between the two real repayment patterns.

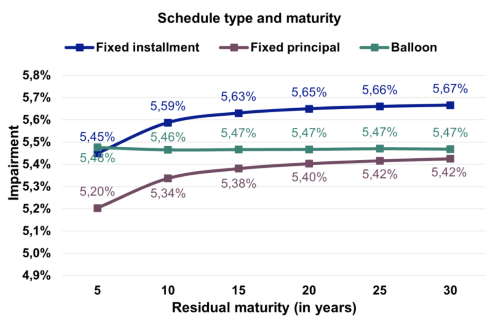

Loss vs maturity date

When analyzing sensitivity, it is also important to look at how the residual maturity affects the loss resulting from loan holiday. The results of the sensitivity analysis in this regard are presented below.

In the case of a theoretical mortgage loan with a balloon payment, the size of the loss remains similar regardless of the residual maturity. For loans with amortizing principal, the loss is smaller the shorter the maturity, with little sensitivity for long tenors of more than 15 years.

The analysis shows that the spread between the loss rate for mortgages with fixed principal-interest installments and fixed principal installments remains at a similar 25 bps, regardless of the remaining maturity. This is illustrated in the graph by the parallel sensitivity curves for these two types of schedule repayments.

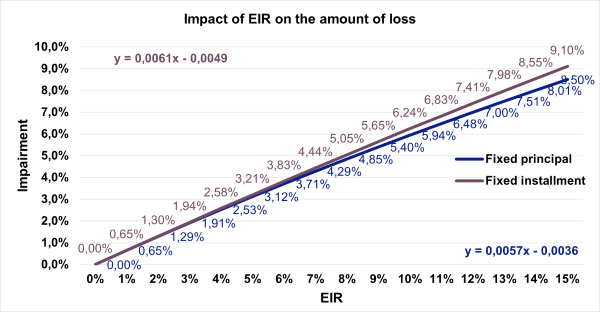

Loss vs effective interest rate

The last significant characteristics being analysed is the amount of the effective interest rate (EIR). Due to the nature of discounting and valuation at amortized cost, the EIR level will be a key driver in creating the amount of loss. The higher the EIR, the greater the loss resulting from loan holiday.

The chart above shows the simulation results for a 20-year loan. As expected, the relationship is almost linear. Roughly speaking, for each percentage of EIR, we "pay" with the loss resulting from the application of the holiday of 0.61% for the fixed installment and 0.57% for the fixed principal installment, respectively (denoted by the regression equations in the chart above).

The above means that the loss will be higher for loans with high margins, high lending commissions and other factors that positively affect EIR.

Date of mortgage holiday

The impact of the timing of the borrower's taking a mortgage holiday was also analysed. All previous analyses were conducted under the assumption that the borrower would use the holiday at the first possible date. For comparison, a variant was verified, in which the customer uses the holiday on the latest possible dates (i.e., in 2022 without October and at the end of the following quarters of 2023). The difference in value loss was negligible at 6 and 7 bps.

Holiday | Fixed princip. instal. | Fixed instalment |

Earliest possible | 5,40% | 5,65% |

Latest possible | 5,33% | 5,59% |

Difference | 0,07% | 0,06% |

What about changes in the ECL?

Previous analyses were focused on the change in gross carrying value (GCV) and its impact on the result. On a portfolio basis, it would be reasonable to assume that as GCV decreases, assuming constant coverage, the amount of the ECL allowance will also decrease proportionately.

However, assumption of constant coverage is a major simplification. ECL change may be significantly disturbed, due to the specifics of the IFRS 9 models used. The disturbance may be due to one or more of the following:

Other aspects

Other questions are also legitimate in the context of holiday: whether and how to allocate to Phase 2 customers using holiday, whether holiday can significantly affect hedge accounting effectiveness tests and securitisations, how to approach the forecast of customers' use of holiday, and how to include them in a liquidity gap analysis.

Above elements can significantly affect the result and should therefore also be examined by the banks, in order to get a full picture of the impact of legislative changes.

If you would like detailed portfolio-specific analyses or support in cross-sectional analyses of the impact of payment holiday, please do not hesitate to contact me.

1 https://www.zbp.pl/aktualnosci/wydarzenia/Koszt-rzadowych-propozycji-to-dziesiatki-miliardow

2 https://www.sejm.gov.pl/sejm9.nsf/PrzebiegProc.xsp?id=5A40FC9AA957CDCBC1258845005DF87F

Solutions to help banks thrive in a complex market

This website uses cookies.

Some of these cookies are necessary, while others help us analyse our traffic, serve advertising and deliver customised experiences for you.

For more information on the cookies we use, please refer to our Privacy Policy.

This website cannot function properly without these cookies.

Analytical cookies help us enhance our website by collecting information on its usage.